{kind=link}

Roy, a financial sector professional with over two decades of banking experience, has been brought in to change the way the non-banking subsidiary of Larsen & Toubro, the eponymous builder of roads and bridges, does business, and make it as nimble and efficient as a fintech.

Despite the parentage of the engineering giant, in many eyes, L&T Finance has yet to distinctly carve out a space of its own in the financing arena. Indeed, the parent, if anything, has been displeased by the middling performance of the lender over the years.

In February 2022, at a press conference to announce that L&T Finance was exiting the wholesale loans business (funding infrastructure and real estate projects), then L&T chairman A.M. Naik had said, “Over a number of years, the only (L&T Group) company which has not performed and is publicly listed is L&T Finance…Our own board members are saying, to me at least, that greater L&T involvement is desirable so that we can drive the ideas and strategies that we want to implement in L&T Finance.”

Naik was not exaggerating.

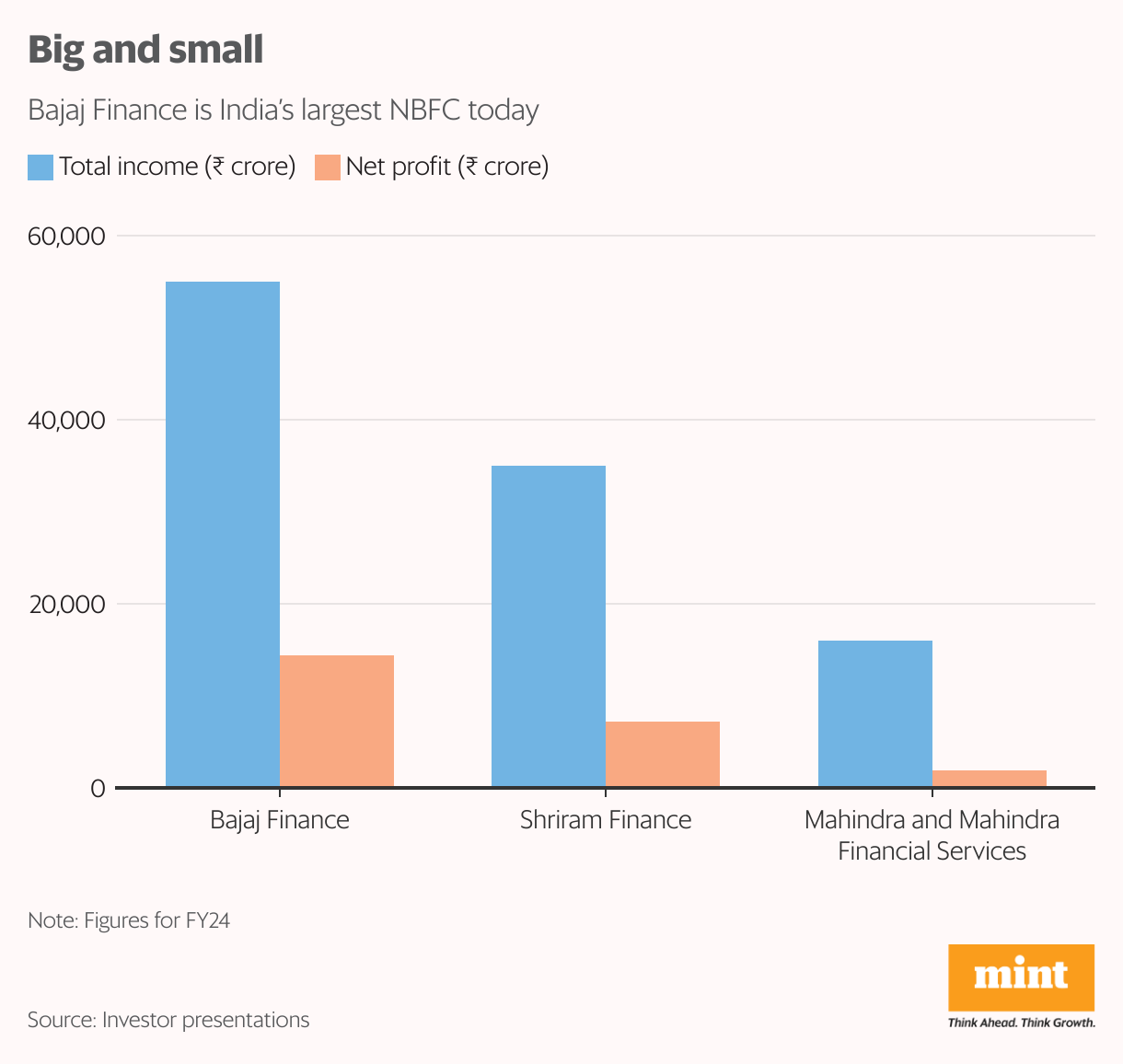

Even after being in business for three decades, L&T Finance remains lower down the NBFC pecking order. Its total loan book, almost all (94%) of it retail (personal, home, two-wheeler loans, etc.), stood at ₹85,565 crore at the end of 2023-24.

Mahindra Finance, which started three years before L&T Finance, in 1991, is well ahead with assets under management (AUM) of ₹1 trillion at the end of the last fiscal year. Bajaj Finance, which started out in 1987 as Bajaj Auto Finance Ltd, an NBFC focusing on two- and three-wheeler finance, has eclipsed them both with an AUM of ₹3.3 trillion as of 2023-24.

L&T Finance’s price-to-book value (a measure that compares a company’s market value to its book value), at 1.97, lags peers Shriram Finance (2.17) and Bajaj Finance (5.68), though it is higher than Mahindra Finance’s 1.83, according to data from Bloomberg. In 2023-24, its return on assets—a key profitability metric—stood at 2.23%, again behind Bajaj Finance and Shriram Finance.

Junking Wholesale Loans

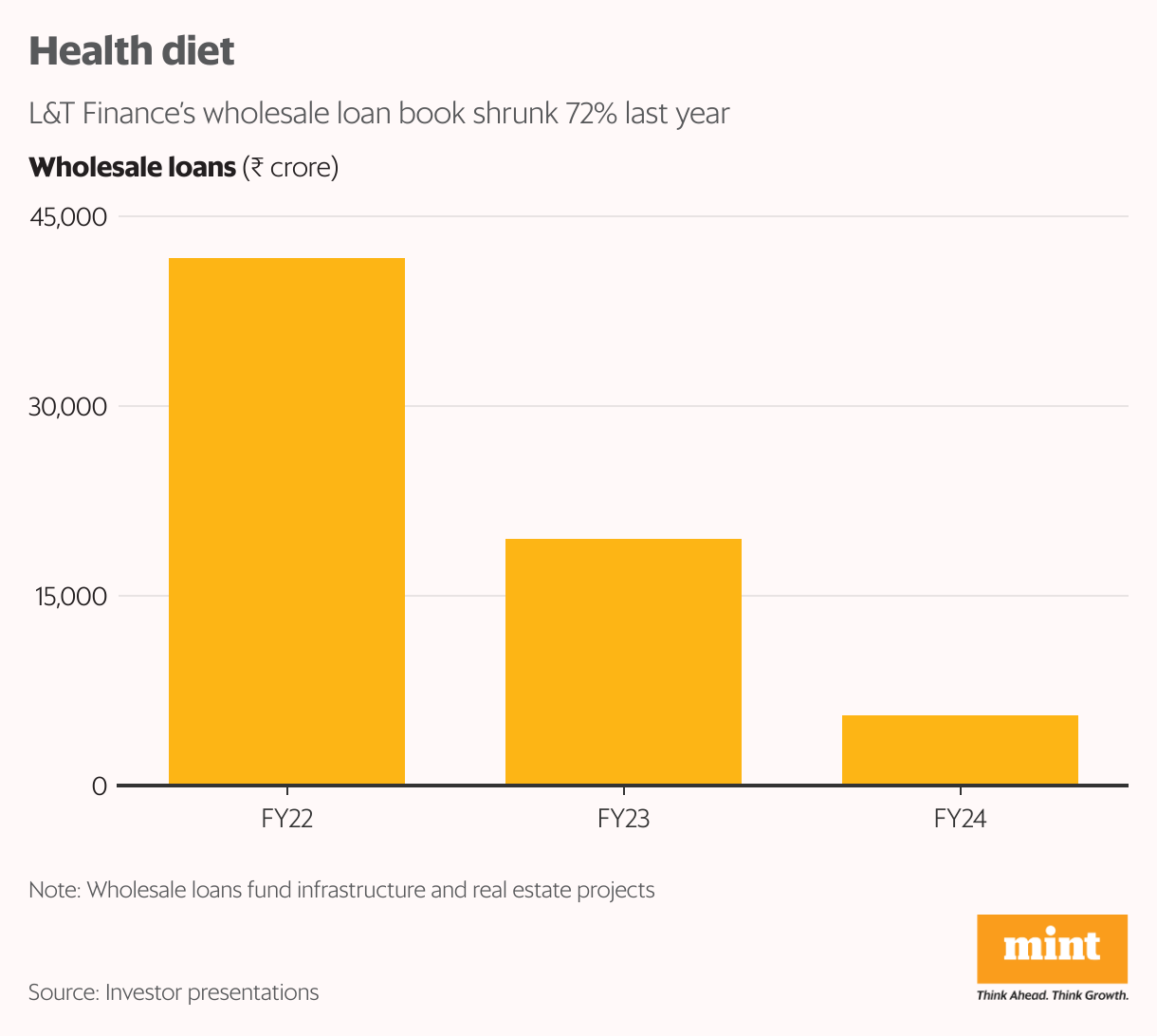

A large part of L&T Finance’s lacklustre performance is being blamed on its earlier focus on wholesale loans. Data from Crisil shows that these loans formed 62% of its portfolio as of 31 March 2016. According to equity analysts, that concentration was a result of the parent’s presence in those segments and the focus of the group as a whole on infrastructure.

In August 2022, not long after the press conference mentioned earlier, Naik told shareholders at L&T’s annual general meeting that steps were being taken to make the NBFC a healthier company. “We had very bad NPAs, particularly in the wholesale and realty businesses. We…are constantly looking for some of these sectors to sell, even if necessary at losses, and concentrate more on retail,” he said.

View Full Image

Clearly, the wholesale business was a bad memory that the group wanted to leave behind as quickly as possible.

In June last year, The Economic Times reported that L&T Finance had invited bids from asset reconstruction companies for non-performing wholesale loans to the tune of ₹3,022 crore, across 10 accounts, mostly in the real estate sector.

As of 31 March, its wholesale book had shrunk 72% to ₹5,528 crore, from ₹19,512 crore in the previous fiscal year. And as of the June quarter of 2024-25, it had been pared to 4.8% of the overall loan book.

While it has had a modest retail book over the years, the company is now concentrating entirely on retail loans. A part of the shift toward retail happened under former chief executive officer (CEO) Dinanath Dubhashi, who retired in April, after spending 16 years at L&T Finance. The group is now banking on Roy, a former consumer banking and payments professional from ICICI Bank, to turn its fortunes around. He joined L&T Finance as its chief operating officer in July 2023 and took over the CEO role in January.

Five-pillar Strategy

“For the first six months, I focused on nothing but business,” said Roy, an avid wildlife photographer whose corner office on the eighth floor is full of photographs of tigers shot on his camera. “Dinanath gave me a free hand. The objective was to streamline the business and focus on performance delivery both in terms of credit cost and topline,” Roy told Mint.

As part of the effort to put the financier on a high-growth trajectory, the management has drawn up a five-pillar strategy, which was announced in October. The five pillars are: raising brand visibility, enhancing customer acquisition, sharpening credit underwriting; building a futuristic digital architecture and building capabilities.

View Full Image

Roy quickly realized that the company needed to improve its brand recall and visibility. “I had noticed something from outside and it was also part of my discussion with SNS (L&T chairman and managing director S.N. Subramanyam) when I was going through the process of coming on board,” said Roy. “I realized that the L&T brand name is reasonably well known and well respected in urban India, but L&T Finance was thought to be predominantly rural.”

The numbers, however, show that L&T Finance’s rural leaning is a matter of perception. Rural and urban retail loans account for an equal share of the bank’s total retail loan book of ₹80,000 crore today.

I realized that the L&T brand name is reasonably well known in urban India, but L&T Finance was thought to be predominantly rural.

—Sudipta Roy

But Roy found that the brand recall and presence in urban areas was “literally next to nothing”.

Brand association is a critical aspect for Roy. While Bajaj Finance is known for its consumer durable finance, Mahindra Finance is associated with financing tractors and Shriram Finance, with used vehicles. L&T Finance, on the other hand, is not associated with any specific aspect. According to Roy, the NBFC’s three fulcrum businesses are micro-loans, tractor finance and two-wheeler finance. He therefore wants the company to be known as a diversified NBFC that “straddles both rural and urban businesses with equal ease”.

Using AI and ML

The new CEO is extremely excited about some of the technological changes at L&T Finance. There is ‘Project Cyclops’ for instance, named after the one-eyed Greek mythological figure, which was announced in a statement last month. A credit risk assessment and automated decision-making digital credit engine, Project Cyclops uses Artificial Intelligence (AI) and Machine Learning (ML) to determine the repayment capability and credit quality of potential customers.

Project Cyclops is a “three-dimensional credit engine” developed internally by a team of 100 developers, said Roy. “Since it was done internally, the cost was about ₹5 crore,” he told Mint.

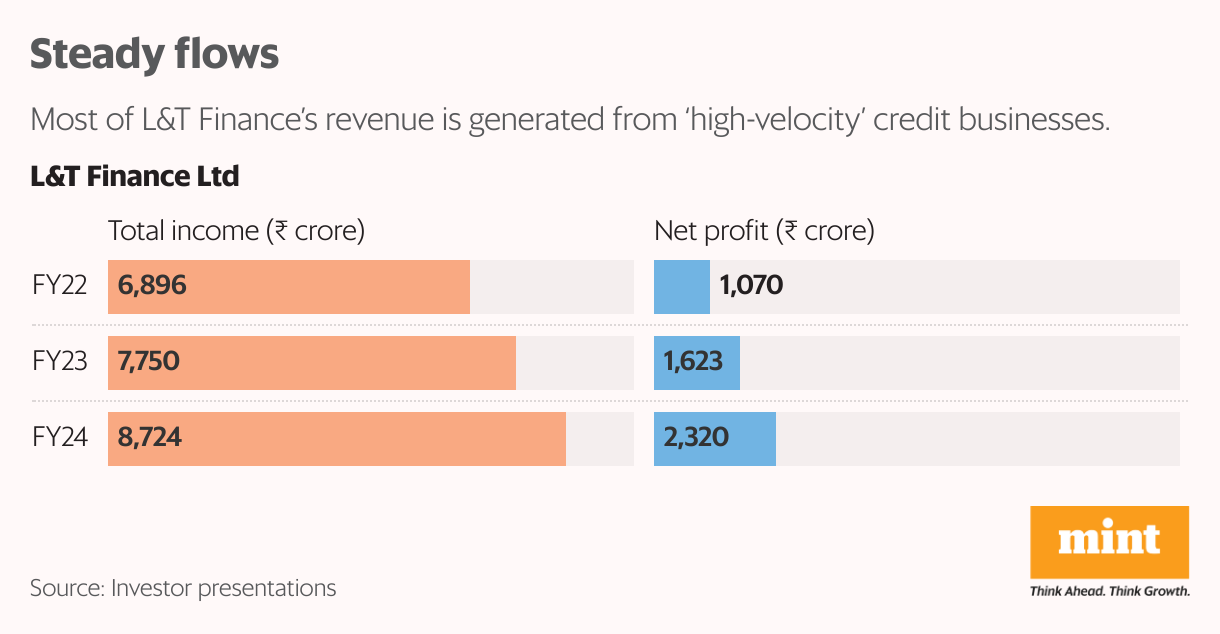

How will it help? He explained that most of L&T Finance’s revenue comes from high-velocity credit businesses where quick decisions need to be made. “For instance, if a customer comes to a two-wheeler dealership and a lender doesn’t finalize whether it will finance within 30 minutes, he/she goes elsewhere,” said Roy. The new credit engine is expected to enable quick and correct decisions on who the company is lending to, especially microfinance customers, and those who are ‘new to credit’ (first-time borrowers).

“Nothing escapes Cyclops,” said Roy. “Our technology team has been working nonstop for the last 45 days to deliver it…We pushed it into beta mode (user testing to identify bugs) on 18 June and are currently using it in 25 two-wheeler dealerships. Over the next 45 days, we will scale it up to 100% of two-wheeler loans.”

After the two-wheeler business, Cyclops will be used in tractor financing, small business loans and finally for mortgages and personal loans. The financier expects Cyclops to improve underwriting standards in the sanctioning of loans.

Decent Start

Have the change in guard and the five-pillar strategy worked? While it is early to say so decisively, there has been a visible improvement in numbers. According to Roy, about a year ago, L&T Finance disbursed between ₹550-600 crore of two-wheeler loans every month; it now clocks ₹900-1,000 crore. Moreover, from 37% in the June quarter last year, the share of prime (better-rated) customers in two-wheeler loan disbursals had grown to 50% by the end of 2023-24.

₹900 crore and 1,000 crore of two-wheeler loans every month. ” title=”L&T Finance disburses between ₹900 crore and 1,000 crore of two-wheeler loans every month. “>

₹900 crore and 1,000 crore of two-wheeler loans every month. ” title=”L&T Finance disburses between ₹900 crore and 1,000 crore of two-wheeler loans every month. “>View Full Image

“It has been going up for close to three quarters now and is serving us well…Our bounce rates (defaults in paying equated monthly instalments) are showing signs of improvement,” said Roy.

In aggregate mortgages and loans against property, it used to do ₹550-600 crore every month; now it does close to ₹900 crore. In rural business finance, the needle has moved from ₹1,550-1,600 crore last year to ₹1,900-2,000 crore per month now.

“We plan to grow our retail book to ₹2 trillion in another four years, by 2027-28,” said Roy. Currently, Federal Bank and Yes Bank have loan books close to this size.

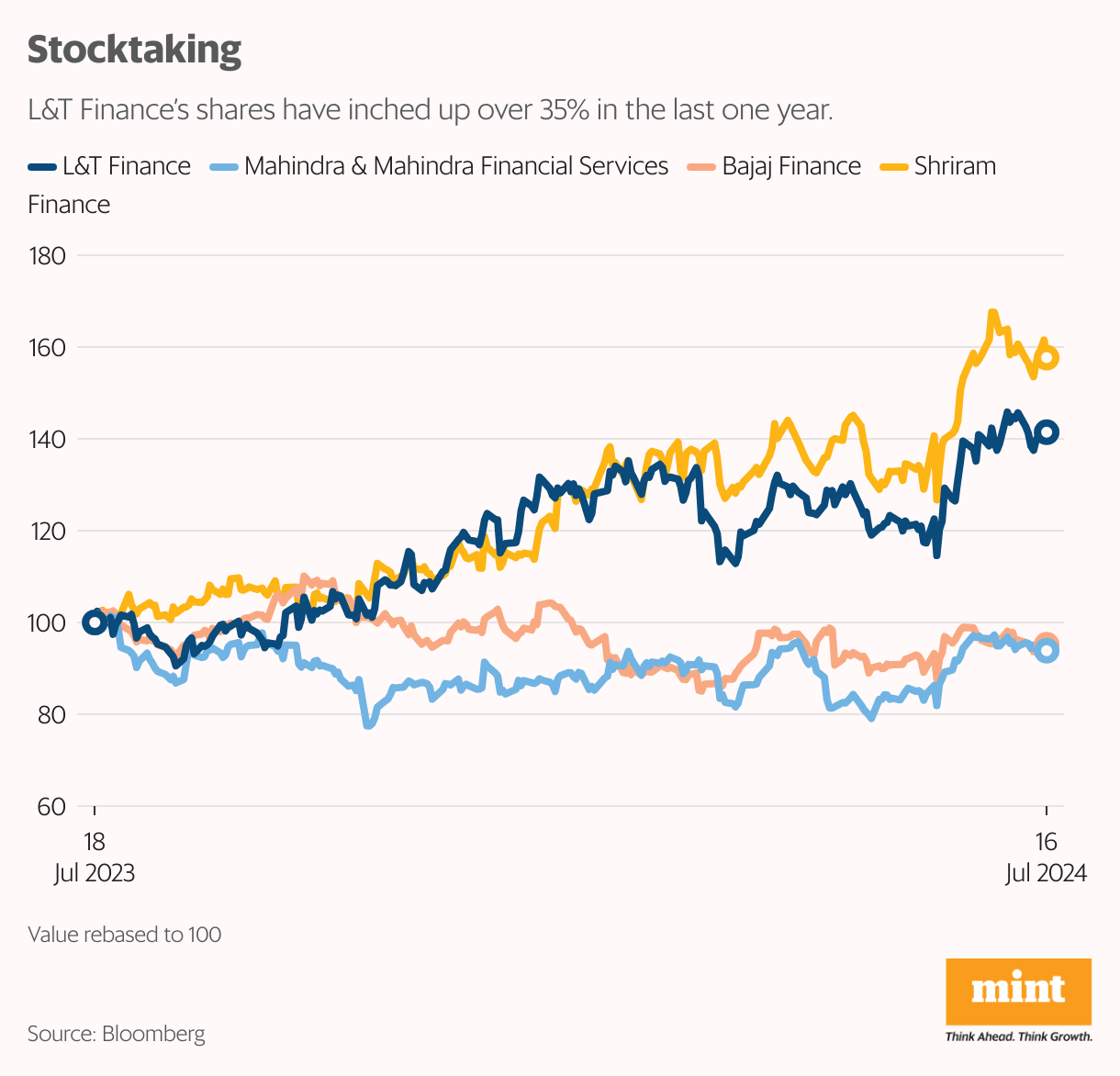

Analysts are upbeat on the company’s push towards retail loans and the move away from wholesale credit. “There have been changes in organization structure, product mix and investments in technology at L&T Finance. We continue to remain bullish on the company and believe all these changes in the organization should eventually lead to balance sheet growth,” said Kaitav Shah, lead BFSI analyst, Anand Rathi Institutional Equities.

Others had similar things to say. According to analysts at JM Financial Institutional Securities Ltd, a combination of factors would allow the lender to report strong returns. These include its shift from wholesale to a high-return retail book; stable asset quality metrics from the thinning of its legacy wholesale book and continuous strengthening of underwriting metrics; and strategic investments in “futuristic technology”.

Tighter Regulation

While aiming for growth, the company also has to navigate a stricter regulatory environment. In September 2022, the RBI classified L&T Finance as an upper-layer NBFC. RBI regulations classify NBFCs into four layers—base, middle, upper, top—based on their size, activity and perceived risks. According to the central bank, once an NBFC is classified as being in the upper layer, “it shall be subject to enhanced regulatory requirement, at least for a period of five years from its classification in the layer”.

The upper layer comprises prominent names such as Tata Sons, LIC Housing Finance and Shriram Finance. For some of the upper-layer NBFCs, the classification came as a challenge since norms mandated them to go public within three years of being identified as one. A few, such as Piramal Capital and Housing Finance, and Aditya Birla Finance, have tried to sidestep it by announcing mergers with their listed parents.

View Full Image

L&T Finance faced a similar problem. While L&T Finance Holdings, the holding company, was listed, L&T Finance, which appeared on the RBI upper layer list, wasn’t. Last December, the company went through an internal restructuring that avoided listing L&T Finance separately.

Under the merger agreement, L&T Finance, L&T Infra Credit and L&T Mutual Fund Trustee were merged into L&T Finance Holdings Ltd (LTFH) and the new entity has also been named L&T Finance.

Roy believes there has been a harmonization of regulations between banks and upper-layer NBFCs. “We do not consider ourselves different from banks. And that is the message that I have given to the team: consider that you are a bank; consider that the same regulatory standards apply to you and consider yourselves to hold the standard that a bank is expected to hold.”

Interestingly, at one time L&T Finance had ambitions of becoming a bank but decided against it after the RBI made it clear that it would not be giving licences to conglomerates.

The RBI raised the level of capital that banks need to set aside for retail loans and loans to NBFCs, raising risk weights by 25 percentage points to 125%.

On another front, the financier will face a challenging environment as the NBFC sector is staring at a slowdown in growth today. Some of this is the result of the RBI raising the level of capital that banks need to set aside for retail loans and loans to NBFCs, raising risk weights by 25 percentage points to 125%, in an effort to curb their growth and lower the systemic risk. According to estimates by rating agency Icra, 2024-25 growth in AUM is likely to moderate to 17-19% in the base case and 14-16% in the stress cases.

“The unsecured consumer loans segment would be the most impacted and may face a sharp reduction in the growth rates in FY25 after many years of sustained robust growth,” Icra stated in April. “On the other hand, LAP/SME & MFI (loan against property/small and medium business and microfinance) loans, which also drove growth in the last two years, would continue to maintain healthy growth,” it added.

That said, Roy is optimistic about delivering the goods. “As a nonbanking financial services company, we are far more agile (than a bank). We are far more nimble and are able to do things much faster.” He has made a steady start, but it will take much more to catapult L&T Finance into the top league.