{kind=link}

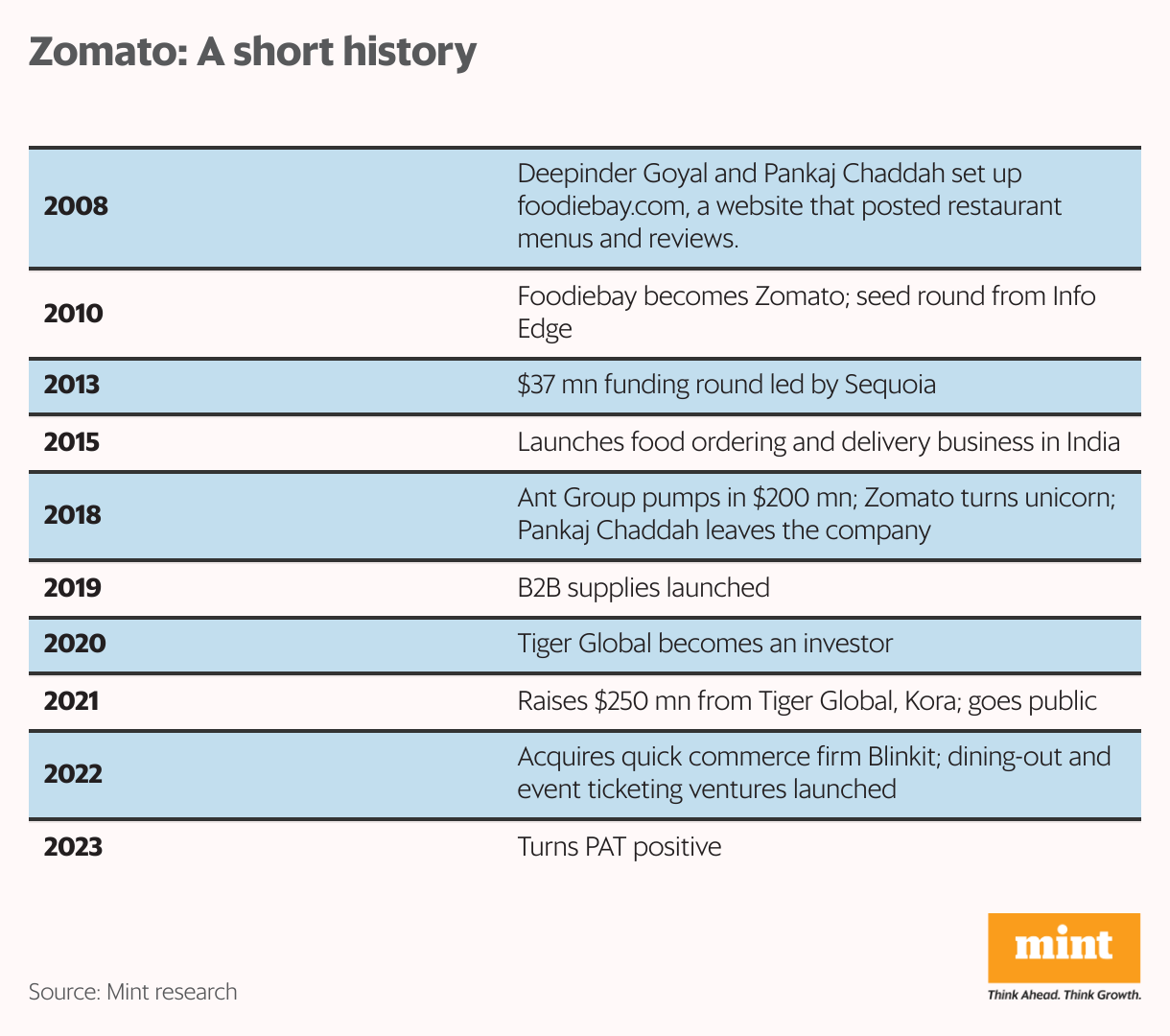

Zomato Ltd, who in its current avatar is both a food delivery and a quick commerce company, stands out. The company’s financials for the fourth quarter of 2023-24 are interesting and mark a turning point in its journey. It reported a consolidated net profit of ₹175 crore for the quarter ending March, which was a 27% sequential growth over the previous quarter. The revenue growth of 8.3% was less than a third of the growth in profitability, which means that the levers of profitability are being unlocked.

These are important indicators not just for Zomato but for the entire venture capital (VC) funded start-up ecosystem.

The year 2021 was seen as the coming of age of startups that were part of a new wave of India’s consumer internet era. A small cohort of these startups, that had broken out into the big league, filed for initial public offerings (IPOs), and listed on the exchanges. Built and scaled with unprecedented amounts of capital, the series of back-to-back IPOs that were enthusiastically received by the markets were proof that this funding model had worked, despite being viewed by the purists with some degree of scepticism.

However, as shareholders began losing money in the aftermath of the listing, the debate on whether startups without a stable revenue model and profits should have been allowed to even list in the first place came up from time to time.

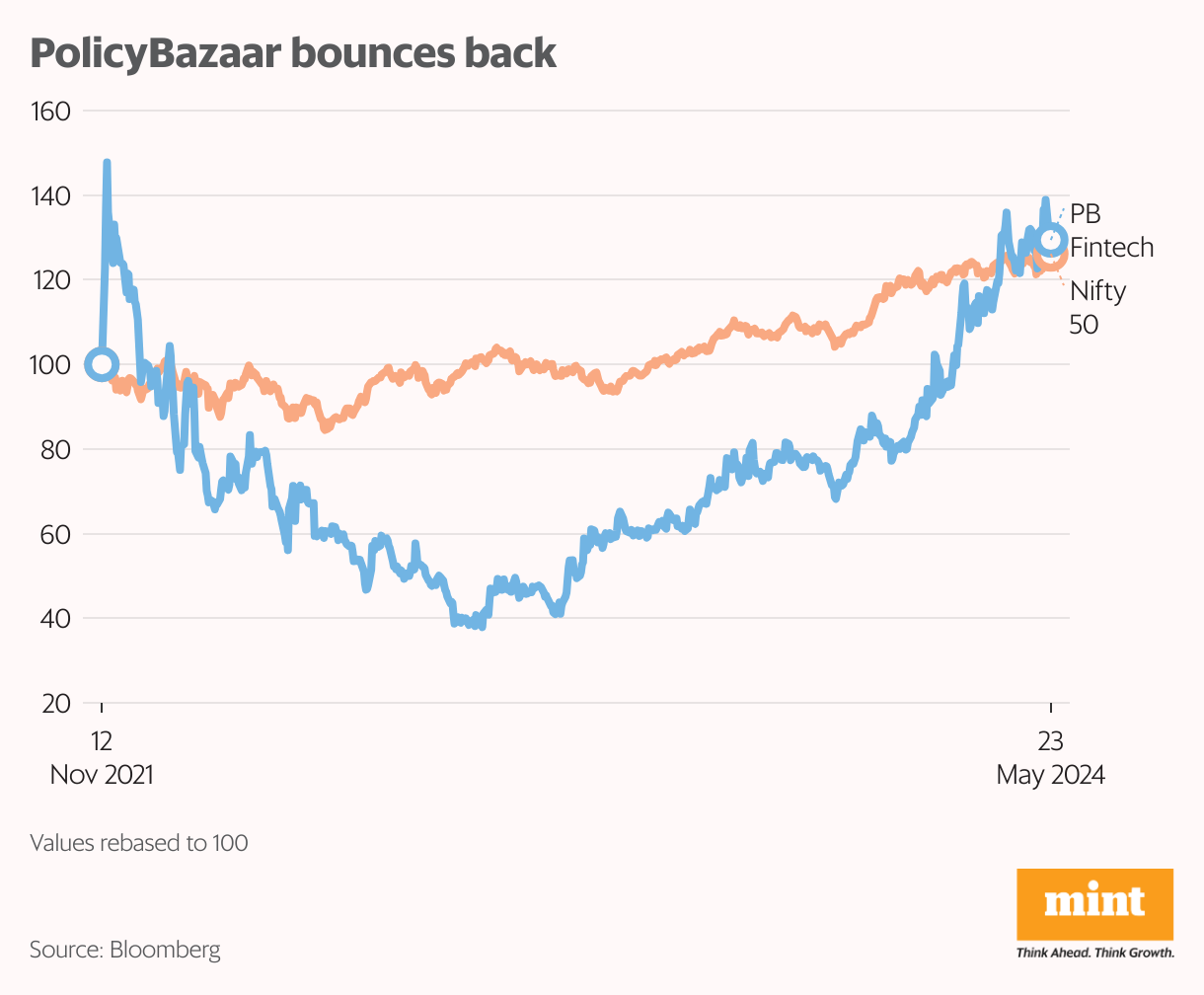

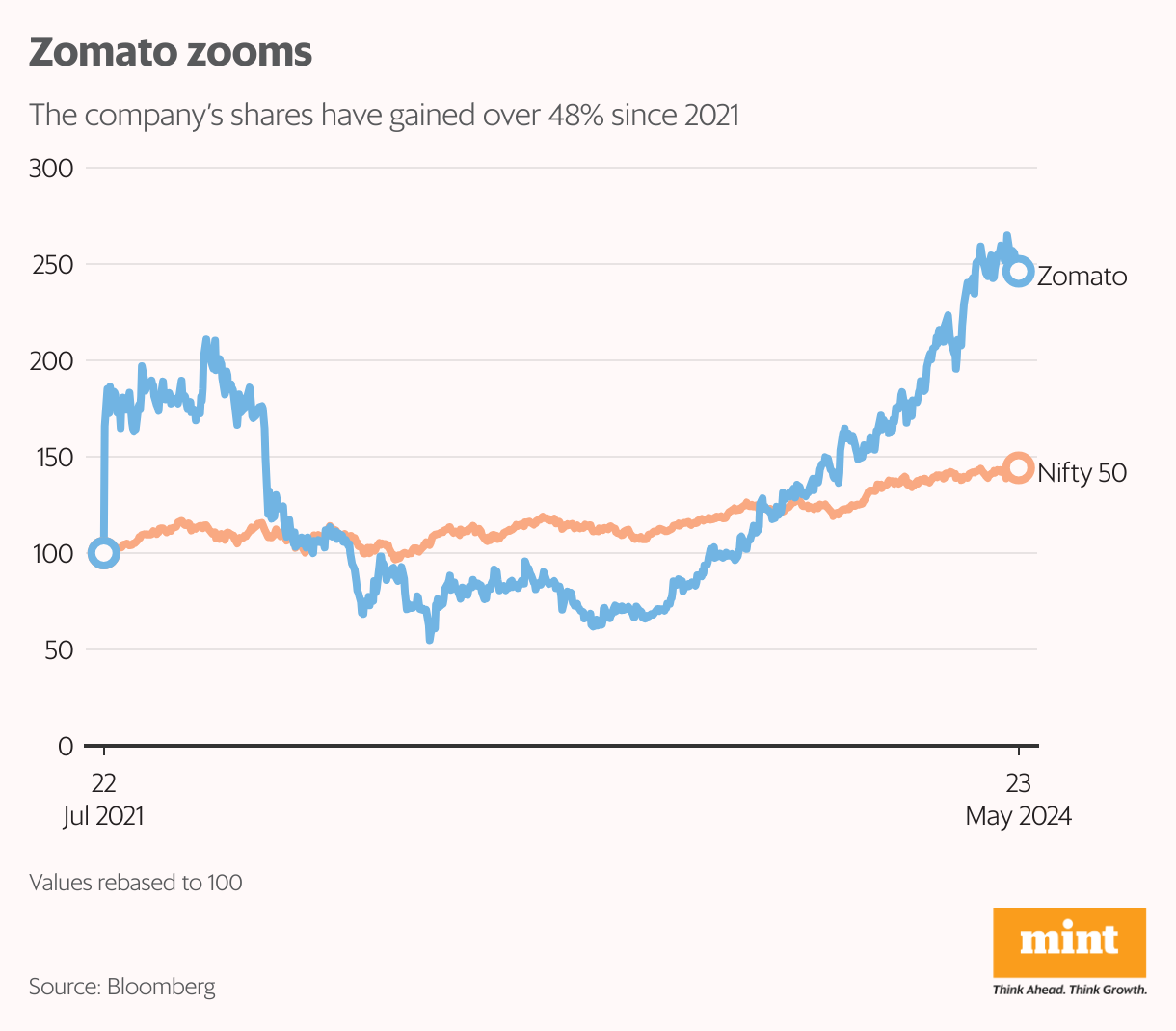

Cut to this year, the gap between the winners and the laggards is now evident and has begun to resemble the last lap of a marathon.

There are some lessons that emerge from the post-IPO journeys of some of these startups, as well as from IPOs that were planned but put off in the eleventh hour.

Big markets + big capital

All the startups that listed in 2021, without exception, were playing in the kind of markets that the VCs love—large total addressable market (TAM).

While a large TAM is a prerequisite for building a big company, it isn’t a sufficient condition. Many other factors—like some form of a real network effect or just simply the extent of superiority of the proposed solution over the current way of addressing the problem—are all equally essential. And even these are not enough. Without a near perfect combination of ‘Clarity, Focus and Execution’ at every stage in the journey, trip-ups and even total collapse are real possibilities.

The assumption that a large problem and an ambitious founder backed by big capital equals a big and profitable company turned out to be a fallacy. Some investors were aware of this fallacy but saying ‘no’ to large-TAM opportunities is seen as suicidal in a game where the human psychology is driven by the fear of missing out (FOMO) on the big opportunities.

To add to the difficulty, it is not easy to predict early in the game as to which of the large problems are amenable to building large and profitable companies and which are the ones that are not. This is partly because many of these businesses required behavioural changes on the part of the customers and it’s not easy to predict what percentage of them would stay hooked to a service or product after the early inducements are withdrawn.

Turns out, Zomato is a winner on all counts. It started off as a ratings platform for restaurants, but quickly pivoted to delivering food, and caught up with rival Swiggy which had a head start in the food delivery business. And food delivery had a strong tailwind of network effect which is more than helpful for scaling a business rapidly.

The decision to acquire Blinkit to catch-up with Swiggy-Instamart on the growing quick-commerce market was an extremely smart move, and Blinkit’s execution under the Zomato umbrella has been quite exemplary.

Zomato stayed maniacally focused on the evolving customer preferences by making timely and relevant strategic choices in terms of new offerings, capabilities, and markets. And above all, keeping a hawk-eye on the execution without being distracted or losing interest.

The lessons

Companies that are struggling to make money with their core product or service but claim, and sometimes even believe, that their large user base will, someday in the future, buy other products and services from them is largely a myth.

Why would anyone who uses a platform for payments, or a platform for tracking and paying credit card bills, be interested in using that platform to buy other products?

And what expertise does a payments platform have in creating insurance products? The platform could at best distribute third party insurance products. And there isn’t a dearth of platforms with high ‘daily active user’ bases like Amazon, Facebook, Google, Flipkart, and Zomato, among others, that could take advantage of their user bases to distribute third party products. None of them have been able to really do this. Distribution and discovery are now commodities with very limited leverage, and value can be captured only in a full stack model where the platform takes ownership for quality and delivery of the service or product.

One would recall the pivot MakeMyTrip had to make from distributing airline tickets to distributing hotel rooms. Airline tickets had little or no margin because the number of airlines were few and didn’t have any trouble distributing tickets through their websites. On the other hand, the small hotels that no one knew about, valued MakeMyTrip’s distribution strength.

View Full Image

Claims of extensive data mining, using sophisticated analytical tools, that would help upsell and cross-sell products, is largely a myth. Your core product or service needs to make money. Some months ago, I had written a piece in which I had compared two different grocery formats, one offline and one online. DMart (Avenue Supermarts Ltd), the offline chain, continues to make money hand over fist simply because of a few smart strategic choices that reflected a deep understanding of what customers really cared about, whereas all online grocery chains that have access to probably terabytes of customer data are struggling to make money.

The tech bogey

View Full Image

In the early years of my professional life, the information technology (IT) revolution (which was really a catch-all phrase for the surge in outsourcing application maintenance and development) had just begun, and it was common for companies unrelated to IT to add the words ‘information technology’ to their names to increase investor interest. In the last decade, the word ‘tech’ has been suffixed to entire domains like financial services, education, food delivery, and property, among others.

Over-indexing on the tech element of the business has often led to inadequate and hasty thinking on the value proposition around the core offering. Fintech startups were taking pride in the use of technology to cut down the time it took to evaluate creditworthiness of borrowers to a few seconds or even a fraction of a second. This is so counter-intuitive when it comes to lending.

When I probed for the secret sauce, everyone pointed to their analytics prowess. When I dug deeper and asked about the underlying logic and algorithms, I didn’t find a particularly mind-blowing response.

Sometime early this year, a VC fund I was advising requested me to assess the founders and leadership team of a fintech startup they were seriously evaluating to fund. It was clear that this startup was much ahead of the pack when it came to key metrics like customer acquisition cost and delinquency rates. Quite obviously, there was something right they were doing. When I probed for the secret sauce, everyone seemed to attribute their success on these metrics to their analytics prowess. When I dug deeper and asked about the underlying logic and algorithms, I didn’t find a particularly mind-blowing response. Suddenly, the dots connected, and I had my kung-fu panda moment: There was no secret sauce. The secret sauce, if there was any, was a strong belief among the entire team around a few fundamentals, namely, the importance of building the business slowly and sustainably, the thoughtful choice of the target customer group (with an income that was high enough to make them credit-worthy but not high enough for the banks to go after) and their steadfast refusal to stray and move to a lower income group to keep growth rates high.

As I was heading out, I asked them why they kept saying that the secret sauce was cutting-edge analytics, when in reality it wasn’t. Their response was interesting: This is what VCs love to hear!

Valuations and execution

View Full Image

Mismatch of startup valuations with the underlying value of the businesses is not uncommon in the world of VC investing especially when a perceived mega trend, or runaway success of an idea in a different market, creates FOMO and drives investing decisions. This is further exacerbated when excess capital chases a limited number of ideas. These mismatches can prevail for long periods of time and tend to get corrected only when it becomes obvious, and the ability to raise further capital at unrealistic valuations diminishes significantly.

Some startups suffered from this syndrome. For those that didn’t have a great product or service, poor execution was like the last nail in the coffin. To me, the collapse of Byju’s wasn’t about poor governance. Poor governance was a consequence of something more fundamental, namely a product that didn’t solve any real problem. And this was compounded by an infusion of big capital that put them on the treadmill, where almost everyone loses sanity and can go to any length to avoid a reality they had worked so hard to hide.

Similarly, the Reserve Bank of India (RBI) strictures that led to the shutdown of Paytm Bank, and a collapse in the share price of One 97 Communications Ltd, Paytm’s parent, was again a culmination of defending an unrealistic valuation. I am not inclined to believe that the Paytm team did not appreciate the seriousness of prior warnings by RBI or the consequences of not fixing the issues highlighted.

I recall a statement made by Ramalinga Raju, after the Satyam scandal had come to light, describing how an initial cover-up for a poor quarterly performance escalated: It was like riding a tiger, not knowing how to get off without being eaten. Paytm’s predicament is more likely reflected in this statement than any kind of brazenness in ignoring the warnings. Defending an unrealistic value is akin to riding this proverbial tiger.

Corrections in valuation can be steep if poor execution or lack of focus and customer centricity around the core business has created niche competitors that are nibbling away at the market share by offering better products and services. For instance, BluSmart, Namma Yatri, and informal communities of well-organized customer centric drivers are relentlessly eating into the market share of Ola.

This correction can become painful not just for the late-stage investors, but even for the early-stage investors because of the protection that liquidity preference clauses offer late stage investors.

It won’t be surprising if some of the start-ups preparing for a listing this year go through a haircut in valuation.

A rapid change in customer preferences can also result in recalibrating the competitive landscape in an industry, and hence the relative valuations of well entrenched incumbents and late entrants, as is happening in the quick commerce space.

Building a highly profitable company can take a long time. Quick commerce at this point of time seems to be a case of too much capital, and too many players, chasing a business that is inherently difficult with capital being the only entry barrier, without any semblance of a network effect. And, in all likelihood, the companies in this space may eventually become profitable but will probably operate at low margins and may never be able to justify the return on capital employed.

It won’t be surprising if some of the start-ups preparing for a listing this year go through a haircut in valuation. And the true test of strength is not about a few quarters of good performance, but about being able to justify and defend a valuation in the long-term and giving good returns to shareholders at every stage.

And finally

It could take decades to build a large and profitable company. And the path is not linear but is littered with many unknowns and uncertainties that could trip up a smooth journey. And as low hanging opportunities start getting scarce and startups begin to address the more difficult problems of customer segments that are money-poor and time-rich, the challenges of building large and profitable companies would keep multiplying.

However, ‘slow and steady’ has never been the operating motto of the VC model and all these ups and downs are par for the course. And in the meanwhile, Zomato can take a bow, and bask in the glory of being the first to reach the finish line.

T.N. Hari is an author and the executive chairman of STEER World.