")

{kind=link}

Justin Paget

Thesis

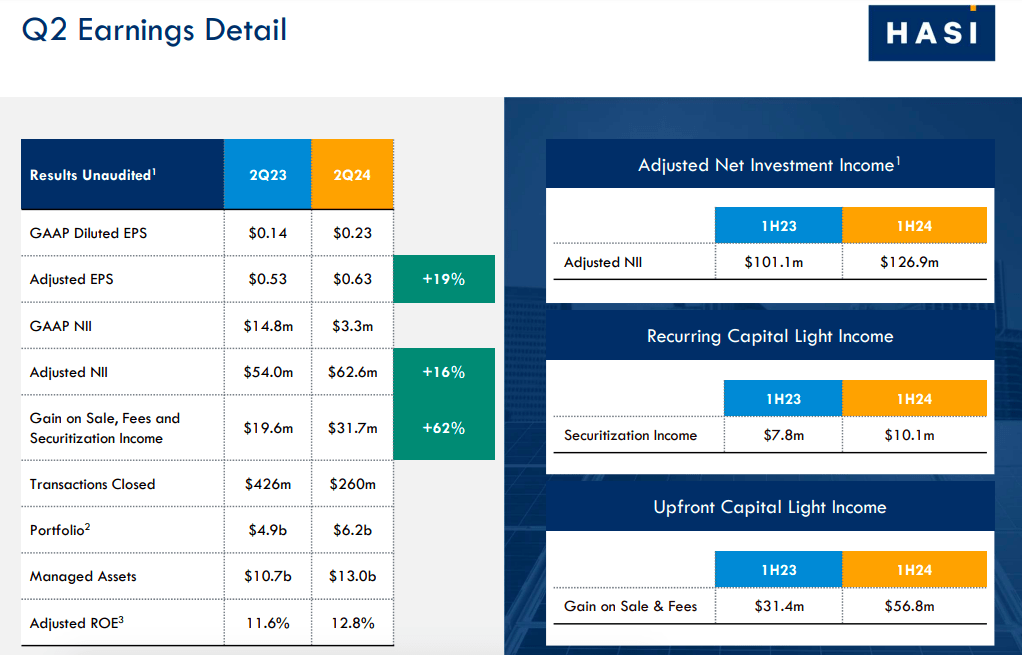

Hannon Armstrong (NYSE: NYSE:HASI) posted solid Q2 2024 results, with Non-GAAP EPS at $0.63, beating estimates by $0.07 and revenue hit $94.52 million. In my analysis, you’ll note that HASI made exceptionally smart moves in climate investments and a growing portfolio keep them ahead in sustainable infrastructure. In my thesis, I argue that even with high borrowing costs, their focus on long-term value and diverse assets sets them up for steady growth in a fast-changing market.

About HA Sustainable Infrastructure Capital, Inc. (Hannon Armstrong)

HA Sustainable Infrastructure Capital, Inc. is a leading investor in climate solutions. It works to create long-term value by financing and managing solutions that unlock the potential of sustainable infrastructure assets, such as renewable energy, energy efficiency, and carbon capture. The company’s portfolio is now valued at $13 billion (combined managed and company portfolio – see below), aiming at the long-term sustainable development of energy, driving them to cleaner forms, and cutting carbon emissions. The overall mission can be describe as investing in a “sustainable future”.

HASI Q2 2024 Earnings Presentation

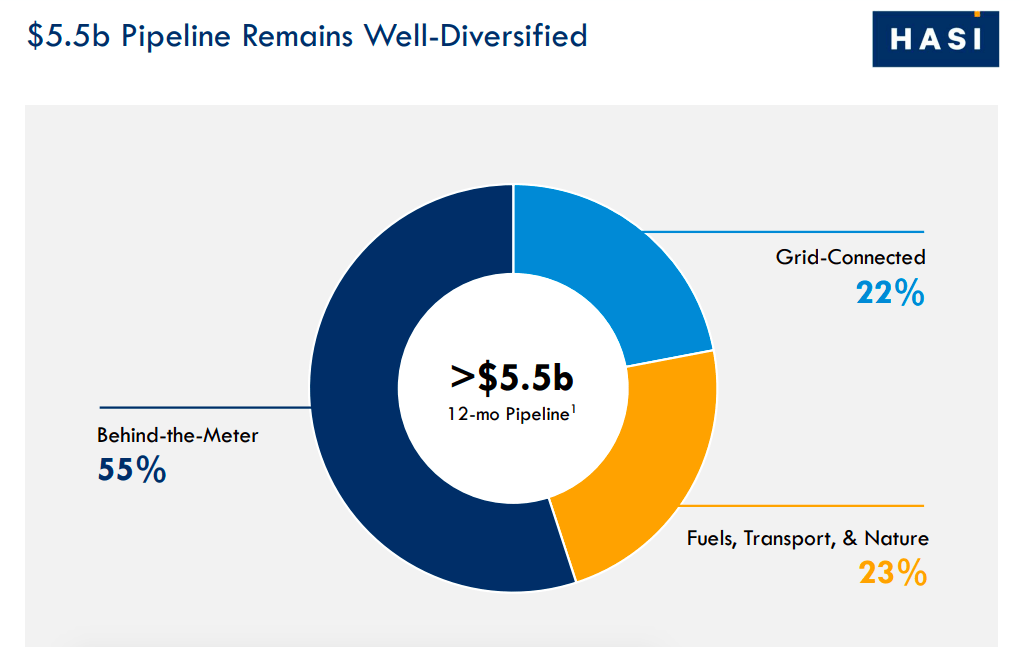

HASI invests in three key areas: BTM projects like energy efficiency and home solar, Grid-Connected projects like wind and solar farms, and Fuels, Transport, and Nature-based solutions like fleet decarbonization and ecological restoration. They use their CarbonCount® tool to measure how much their investments cut down on carbon.

HASI Q2 2024 Earnings Presentation

Essentially, HASI operates like a real estate investment trust (REIT) with specialized focus on the aforementioned climate solutions and sustainable infrastructure. Here are some core aspects of HASI’s business model:

Climate-positive investments: HASI invests in projects that reduce or offset greenhouse gas emissions. Its portfolio includes renewable energy (such as solar and wind farms), energy efficiency upgrades, and other climate-positive infrastructure (This is where the proprietary CarbonCount® tool is used to decide how many tons of carbon are reduced by each dollar invested in a particular project).

Diversified Asset Portfolio: HASI invests in a spread of portfolio of projects, including residential solar, wind and solar farms and ecological restoration projects, to diversify risk and concentrate investment in areas with the highest environmental returns.

HASI’s Revenue Streams:

HASI Q2 2024 Earnings Presentation

HASI makes money in a few ways:

Net Investment Income: These arise from the long-terms contracts that they have linked to their assets

Gain-on-Sale Securitization ($31.7m in Q2): Because they often sell some of their assets but retain some of the cash flows, their investments effectively turn into cash.

Asset Management Fees ($13b in Q2): They can also earn fees from managing others’ assets or offering them advice, particularly for institutional investors.

Strategic Partnerships: HASI partners with other banks, asset managers and corporations to co-invest in large-scale sustainable solutions. For example, HASI partnered with KKR to invest $2 billion in sustainable infrastructure, leveraging its capabilities and capital to expand climate solutions.

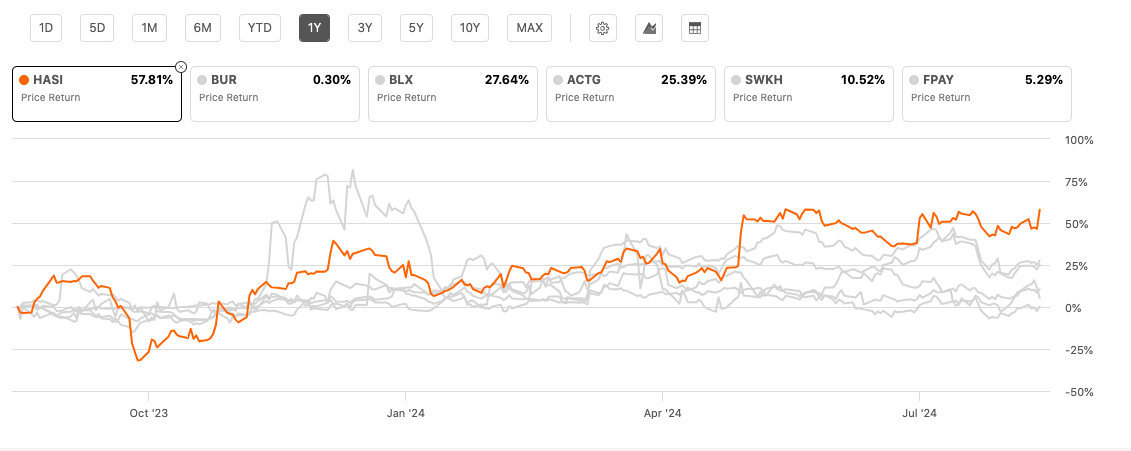

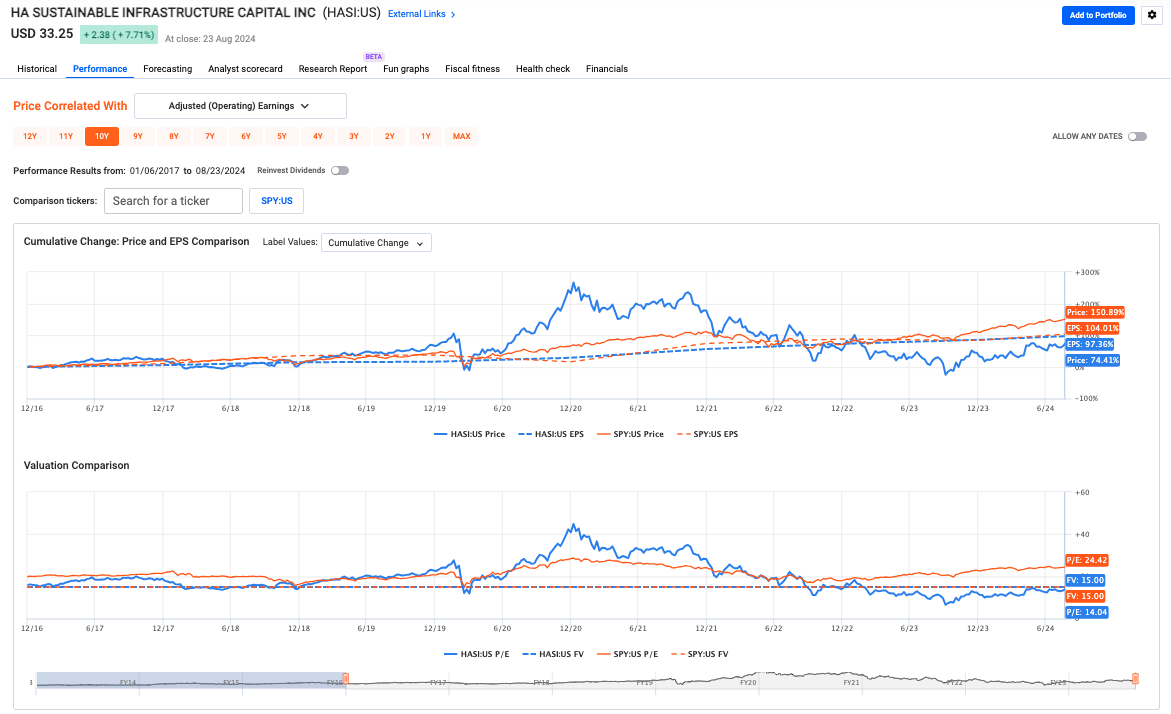

HASI’s Performance

Seeking Alpha

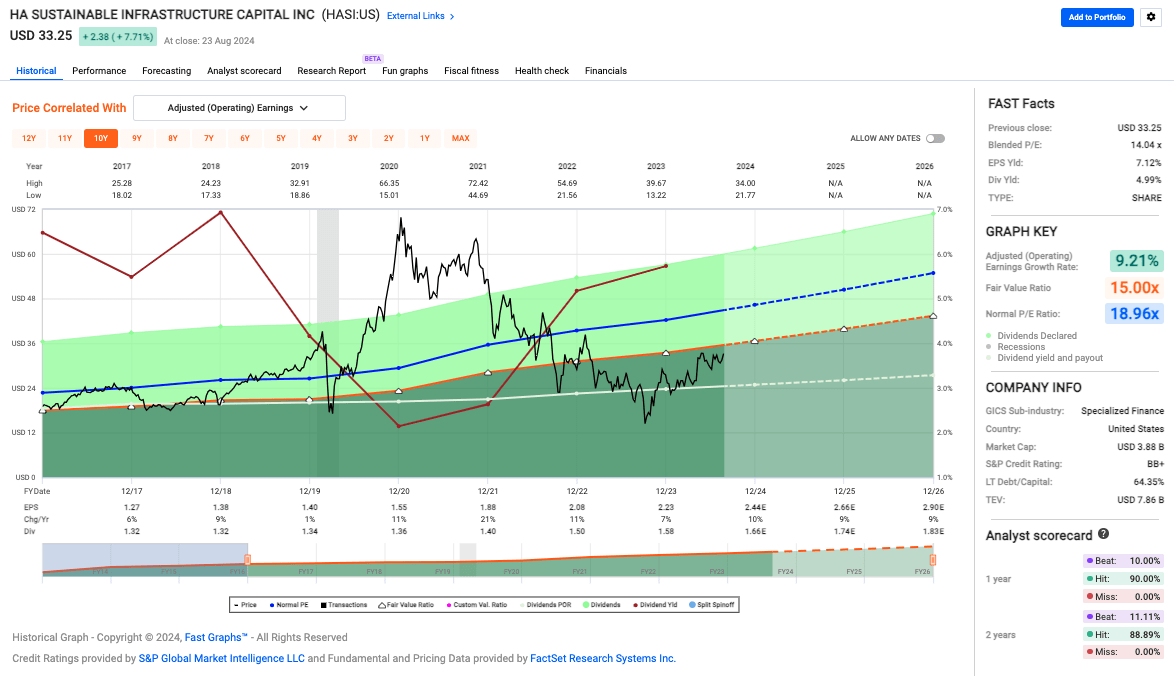

Compared to its peers, HASI is by far the leader with a 1Y 58% price return.

Fast Graphs

And since the beginning of 2017, HASI’s stock went from $19.51 to $33.25 by August 2024. That’s not too shabby, but it’s not keeping pace with the S&P 500. HASI’s return without dividends was 7.24% compared with 12.61% for the S&P 500. Holding its own against its peers? Definitely. Keeping pace with the broader market? No. That could be a warning for growth-focused investors.

Dividends

Fast Graphs

For HASI, dividends have seen a steady increase, but nothing flashy: The average growth rate over the last eight years is 4.95% (the S&P 500 is 5.92%). Because the dividend payout ratio is better now than in 2017 (when it was above 100%—that is, they paid out more than they earned) it’s gone down to 70.85% in 2023, which is still a sizable figure and illustrates the fact that HASI is a company that likes dividends.

Taken together, dividends and stock price growth for HASI produce mild but steady returns. The total compound growth rate, including dividends, is 11.22%. Not terrible, but not S&P 500 territory, which has a total compound growth rate of 13.71%, which may be a little too tame for growth-seeking investors.

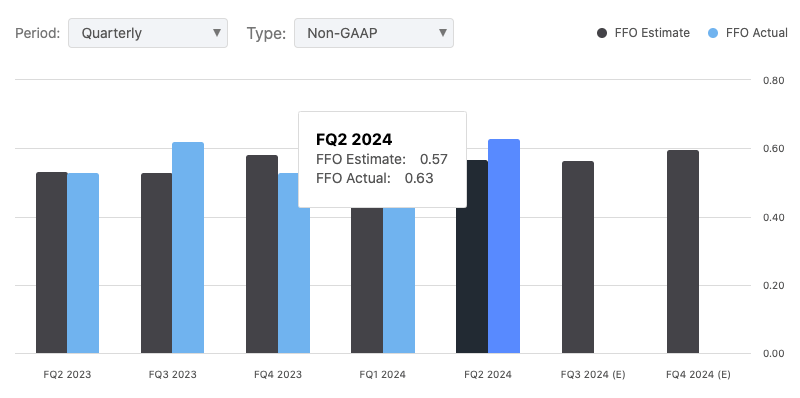

Hannon Armstrong’s Q2 2024 Earnings Highlights

Hanon Armstrong Sustainable Infrastructure Capital, Inc reported strong Q2 2024 results, with adjusted earnings climbing 19 % from last year to $0.63.

Seeking Alpha

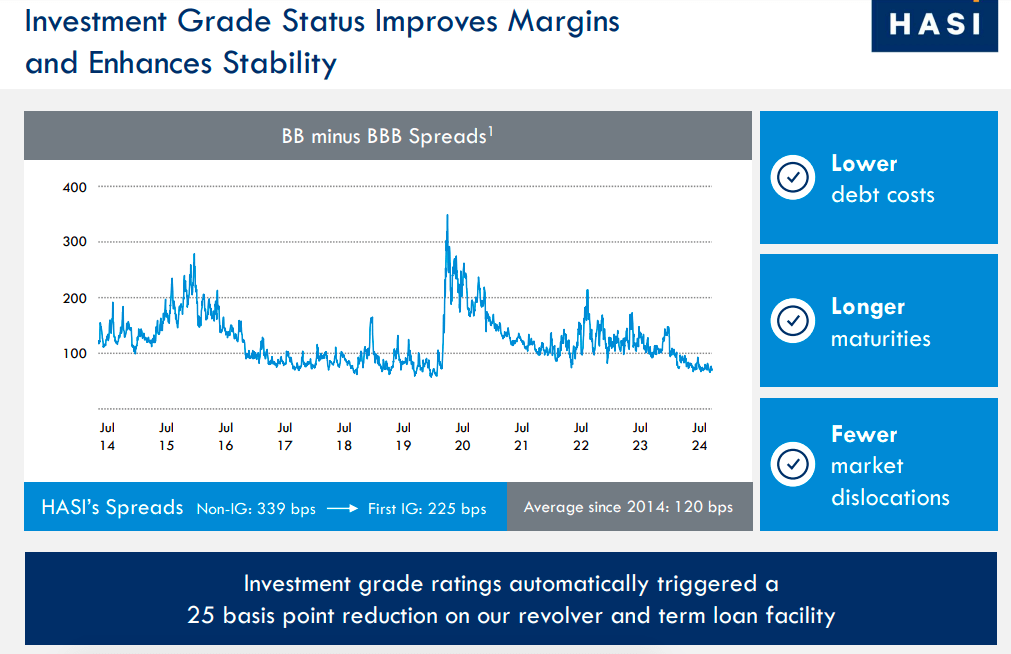

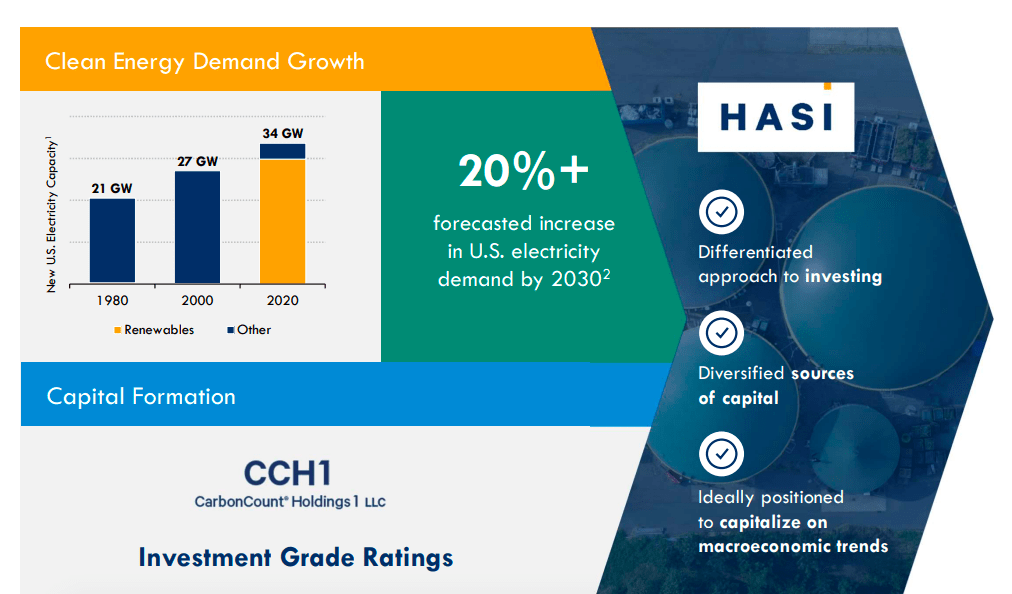

Also, HASI had scored a second investment grade rating, courtesy of Fitch, and S&P put them on positive watch which will help their financial strength and cut capital costs.

HASI Q2 2024 Earnings Presentation

With this investment-grade rating, HASI now has longer duration capability, which is great with lower rates. When asked if this change will alter their approach to debt at the board level—in other words, whether they would consider using more debt since it’s cheaper and available for longer, or if their overall approach to leverage will stay the same—the response was clear.CEO, Jeff Lipson said there would be no change. He noted:

The rating agencies are strict about leverage. To keep our investment-grade rating, we need to maintain current leverage levels. We’re not looking to increase leverage. The only difference, as Marc mentioned, is the lower cost and longer duration.

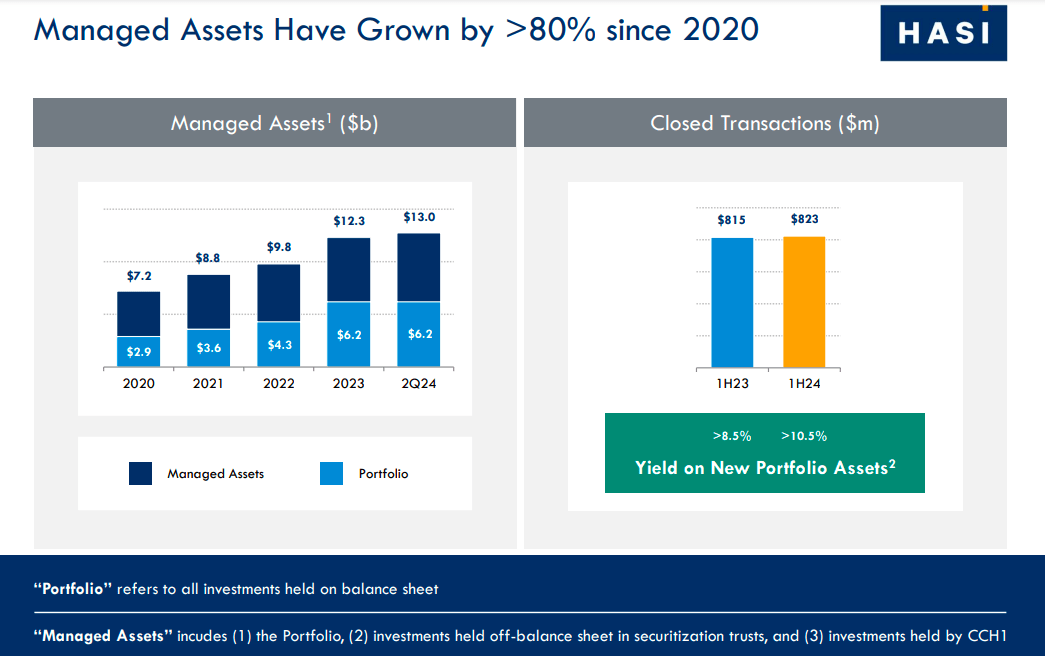

The company’s portfolio jumped to $6.2 billion, up 27% year-over-year and managed assets soared over 80% since 2020, hitting that $13 billion I noted earlier. New investments brought in over 10.5%, up from 8.5% earlier in 2023, showing Hannon Armstrong’s knack for locking in high returns.

A key win this quarter was closing that $2 billion deal with KKR I mentioned earlier which boosts capital access, diversifies revenue, and slashes capital needs by 50%. When asked about the 20% year-over-year growth in managed assets and how the KKR partnership might impact it. CFO Marc Pangburn explained that the recent asset transfer to CCH1 (CarbonCount Holdings) was a one-time deal to kick off the partnership. Going forward, new investments will go straight into CCH1, with no need for more transfers. He added that managed asset growth depends on the deals they close each year, whether those deals end up in their portfolio, in CCH1, or get securitized. All these factors drive the overall growth of managed assets.

HASI Q2 2024 Earnings Presentation

Moreover, with rising demand for clean energy, fueled by AI-driven data centers (according to management, they’re expected to become 8% of U.S. electricity consumption by 2030) and electric vehicles, Hannon Armstrong seems ready to seize these opportunities within the shift from the oil markets to the electricity markets. On the green front, their renewable energy investments cut about 8 million metric tons of CO2 each year.

Looking ahead, the company stuck to its goal of 8% to 10% adjusted EPS growth from 2024 to 2026 and they’re aiming for a 50% payout ratio by 2030.

Finally, financially, the company trimmed its cost of debt to 5.6% in Q2 2024, despite rising interest rates. They started the second half with $1.4 billion in liquidity, ready to back their investments.

HASI Valuation

HASI’s current (blended) P/E ratio is 14.04x, which is below the usual 18.96x suggests to me that the stock might be undervalued, either that or investors are just nervous about future growth. But when I see an earnings growth rate of 9.21%, it looks like a solid buy for those seeking growth without paying too much.

Fast Graphs

Add to that a 7.12% earnings yield makes the stock even more attractive. When I compare this to the 4.99% dividend yield, it shows that HASI is making plenty to keep paying dividends which is good news for investors who rely on steady income.

Also, with the fair value ratio of at 15.00x it could be a catalyst for some upside, but, keep in mind, the stock might be nearing its true value with a market cap of $3.88 billion and a total enterprise value of $7.86 billion, the market could be pricing in both growth and the management of its debt.

Risks & Headwinds

HASI Q2 2024 Earnings Presentation

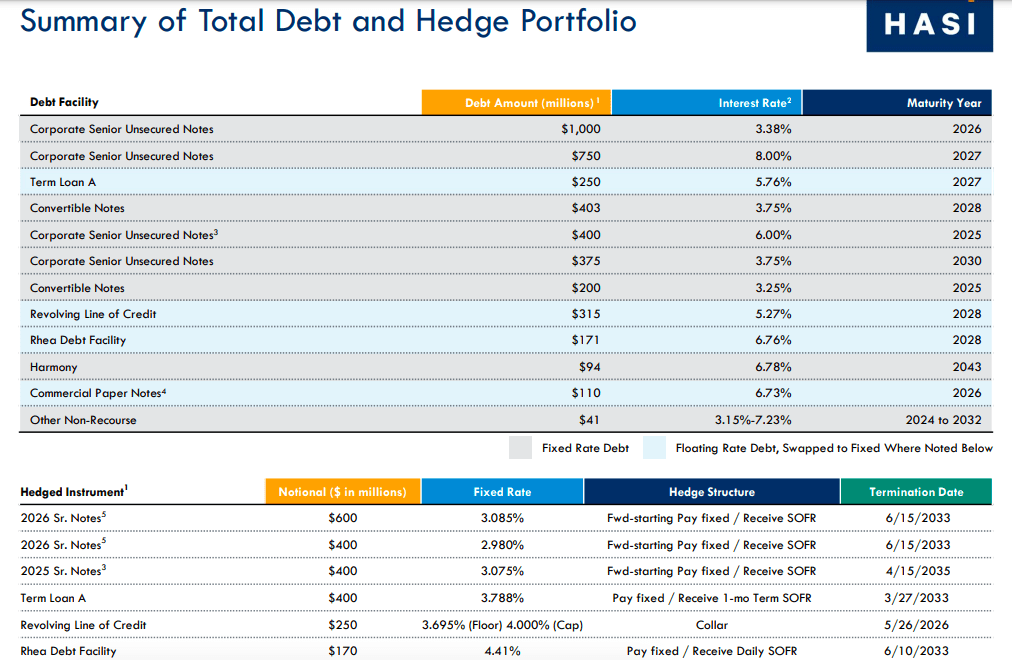

Hannon Armstrong faces some tough hurdles as borrowing costs are still high, with past high-yield debt carrying a 339 basis point spread. The company’s success hinges on clean energy demand and good market conditions, but policy changes (upcoming election) or other external factors could shake things up so even though they’ve handled interest rate risk well, the high-interest rates continue to be a challenge. Although, for context, the cost of debt is up compared to 2023 but it dropped to 5.6 from 5.7 in Q1 2024.

Hannon Armstrong cut its leverage ratio to 1.8x, but that’s still a lot of debt and if the market goes south, it could be trouble (long-term debt to capital ratio is at 64.35%). The $12 million jump in securitization income this year? Selling lower-yield investments to buy higher-yield ones sounds good, but it’s risky.

HASI Rating

I’m giving the stock a ‘Buy’ rating. The financials are good, the growth story is good, and the sector and company are well-positioned for long-term growth in clean energy. Yes, its cost of borrowing is elevated, but in my opinion its move toward long-term value, its steady diversification of its portfolio of assets, and its new investment-grade rating all portend steady growth and income.