{kind=link}

Alphabet (NASDAQ:GOOGL) has turned the heat up in its conflict with the Justice Department, pushing back on its remedy proposal.

Don’t Miss Our Christmas Offers:

Last week, Alphabet submitted a counterproposal arguing that the DOJ’s remedy plan exceeds the scope of the original case and Judge Mehta’s ruling. Alphabet also claimed that the proposed remedy would negatively impact American consumers. The company reiterated its commitment to innovation, claiming its market leadership is down to the quality of its services rather than coercion or a lack of alternatives. Additionally, Alphabet pointed out that advancements in AI have significantly transformed the industry since the trial, with new players further increasing competition.

BofA’s Justin Post, an analyst ranked in the top 1% of Wall Street stock experts, anticipates these claims will form the foundation of Google’s remedy case, which is scheduled for trial in April, with a decision expected by August.

As for Google’s remedy proposal, it includes several measures aimed at addressing competition concerns. The company suggested revising its current search distribution agreements with partners like Apple and Mozilla to be non-exclusive. This would allow partners to enter into multiple default search engine deals across different platforms and browsing modes, such as setting separate defaults for iPhones and iPads. Partners would also have the option to switch their default search provider at least once a year. Additionally, Google proposed retaining revenue-sharing agreements with browser developers and device manufacturers. For device makers, the company suggested allowing the preloading of multiple search services and unbundling services like the Play Store, Chrome browser, and Google Search.

“As expected,” commented the 5-star analyst, “Google’s proposal would be a more positive potential outcome vs DoJ proposal, with the key clause being maintenance of revenue sharing, which we think would give Apple and other OEMs incentive to stay with Google for search. However, we note that Google’s proposal could open the door for greater competition on mobile devices from existing app and browser competitors, and new AI entrants (such as AI browsers or assistants on Samsung).”

Judge Mehta is anticipated to rule on remedies in August, a decision that could significantly influence sentiment regarding Google’s “long-term search revenue opportunity.” That said, Post thinks a potential shift in DOJ leadership under the incoming administration or outcomes from appeals could alter the trajectory of the case or even lead to a settlement. Meanwhile, media outlets have been reporting that Google founder Sergey Brin and CEO Sundar Pichai recently met with President-elect Trump.

In any case, Post keeps a positive stance here. “We remain constructive on Google’s opportunities with AI. Our checks suggest roll out of ads in AI Overview is creating a possible tailwind for top ranked ad in commercial queries, while we think there could be more ad opportunities for informational queries down the road,” the analyst summed up.

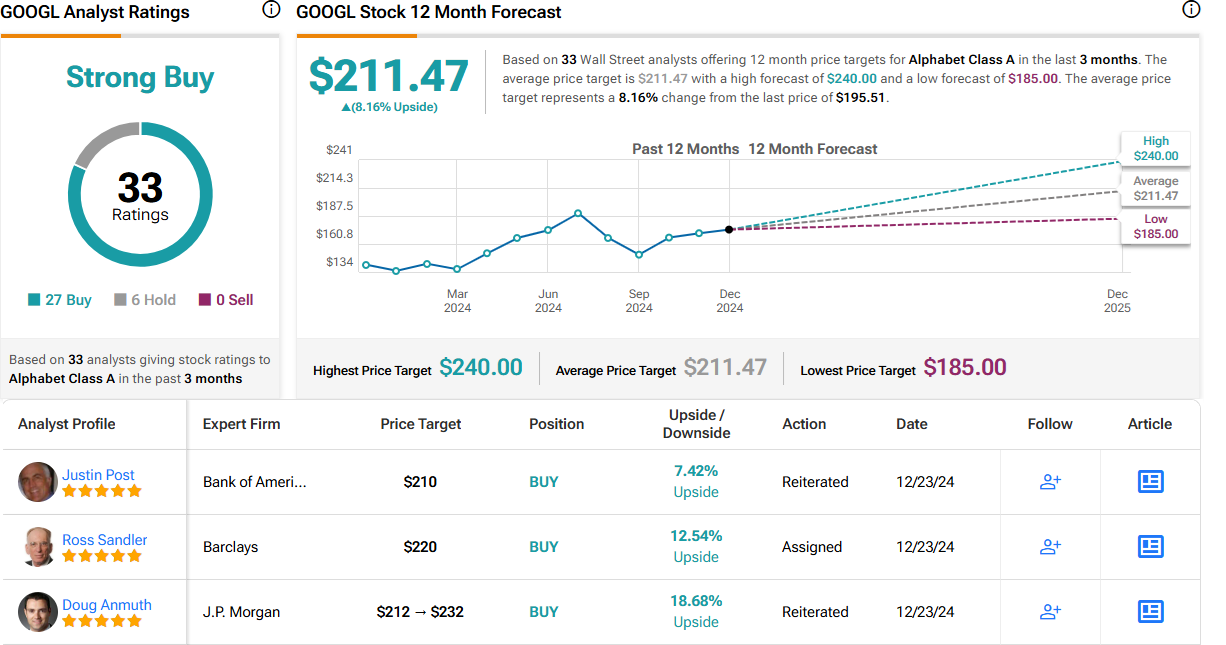

All told, Post maintained a Buy rating on the shares backed by a price objective of $210. There’s potential upside of 7.5% from current levels. (To watch Post’s track record, click here)

26 other analysts join Post in the bull camp while an additional 6 Holds can’t detract from a Strong Buy consensus rating. The $211.47 average target is only slightly higher than Post’s objective. (See GOOGL stock forecast)

{kind=link}

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.