: Explosive Google Cloud Growth Mispriced by Wall Street – TipRanks.com")

{kind=link}

While Wall Street reacted positively to Alphabet’s (GOOGL) Q3 results, I believe shares remain undervalued, presenting a compelling opportunity today. Alphabet’s core business segments, like Google Search and YouTube, remained robust and displayed impressive growth in Q3. However, the true highlight of the report was Google Cloud, which not only recorded a notable acceleration in revenue growth but also saw substantial operating income gains. Yet, Alphabet’s valuation doesn’t seem to fully reflect its ongoing momentum. For this reason, I remain invested in Alphabet, confident about the potential for upside in the stock.

Google Search and YouTube Keep Dominating

Alphabet’s core revenue segments, Google Search and YouTube, once again posted solid numbers in Q3, reinforcing the company’s position as a digital advertising and search leader. Although I hear concerns from investors and analysts about Alphabet’s lagging position in the large language model (LLM) search arena, the company continues to attract increasing advertising revenue.

Specifically, Google Search saw a 12% revenue increase year-over-year, with management citing growing user engagement fueled by recent AI tools like AI Overviews and Circle to Search. AI Overviews has now been rolled out to over a billion users worldwide, enabling more complex queries and expanding how people interact with Search. Circle to Search, another AI feature that lets users draw a circle around an object in an image to search for similar items directly, is now active on over 150 million Android devices.

The Circle to Search feature has been quite popular. Management reported that one-third of those who have tried it are now using it weekly, which translates to a strong indicator of its value.

Meanwhile, YouTube recorded a 12% growth in ad revenue, driven by brand and direct-response ads. The platform’s progress in creating a more TV-like experience, including features like multiview, has definitely boosted its appeal, particularly in the living room space. Shorts is also doing really well, with monetization getting stronger again this quarter. It’s interesting to see how quickly it’s catching up to the in-stream video, especially in the U.S. and other high-ad revenue markets. Notably, 70% of channels uploading to YouTube each month post Shorts, helping Alphabet pull in even more ad dollars.

Google Cloud Impresses with Accelerated Growth and Profitability

Beyond Alphabet’s core segments performing well, the real standout in Q3 was Google Cloud, a major driver of my bullish outlook on the stock. The segment saw its revenue surge by 35% year-over-year, accelerating from the prior quarter’s 29% growth and well above last year’s 22%. This acceleration is powered by Alphabet’s ever-growing AI infrastructure, including the Gemini models, which power solutions in multimodal AI and real-time analytics.

Although these tools may not yet resonate widely with everyday consumers, which might explain why some perceive Alphabet as lagging in the space, they are being adopted rapidly by major commercial clients. Noteworthy examples from Q3 include Snap (SNAP) and Hiscox (GB:HXS). In Hiscox’s case, the company was able to reduce the time needed to generate complex insurance quotes from days to just minutes. I think this shows Alphabet’s real potential to drive revenue by creating value for its customers. As its AI tools help businesses run more efficiently and cut costs, more clients will likely be willing to pay for the benefits they’re seeing.

But more importantly, Google Cloud is gradually growing as a profit generator for the overall business. Its operating income surged from just $266 million a year ago to $1.9 billion. This huge boost in profitability reflects Alphabet’s success in achieving economies of scale, with the operating margin in the Cloud segment climbing to 17% from 3.2% last year.

Valuation: Wall Street Ignores Superb Top and Bottom-Line Growth

Despite Alphabet’s impressive Q3 results, Wall Street seems to undervalue the stock. Particularly, Alphabet is trading at just over 21 times the consensus $7.99 EPS estimate for 2024, a rather low multiple given its accelerating revenue and earnings growth, especially in Cloud. Looking further ahead to 2025, Alphabet’s forward multiple drops to around 19 times expected earnings. I believe this makes for a rather attractive valuation compared to the broader S&P 500 (SPX), where many companies trade at much higher multiples with considerably weaker growth prospects. There have been few opportunities historically to buy Alphabet at a sub-20 P/E, and each time, in hindsight, it has proven highly rewarding.

Is GOOGL Stock a Buy, According to Analysts?

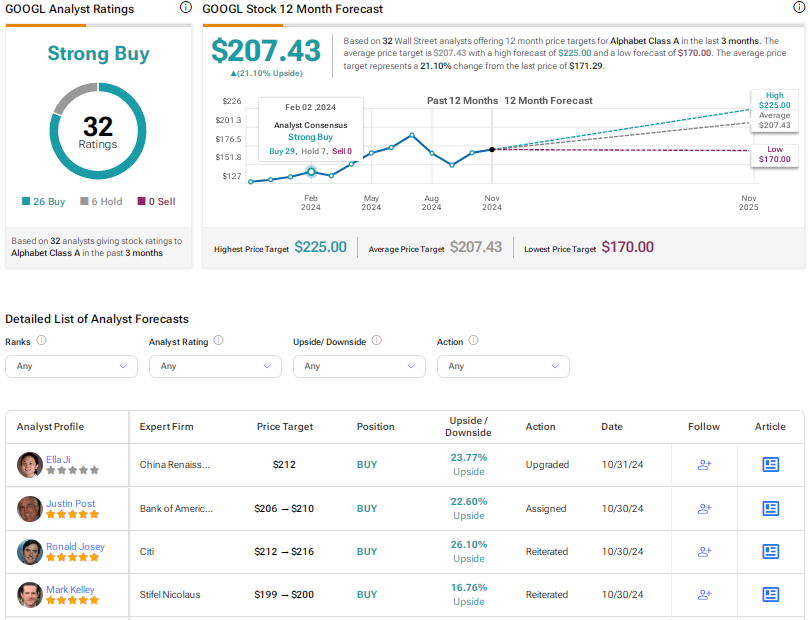

Looking at Wall Street’s view on GOOGL stock, Alphabet features a Strong Buy consensus rating based on 26 Buys and six Holds assigned in the past three months. At $207.43, the average Alphabet stock price target suggests 21.1% upside potential.

If you have yet to choose which analyst you should trust if you want to trade GOOGL stock, consider Mark Kelley from Stifel Nicolaus. He is the most profitable analyst covering the stock (on a one-year timeframe), featuring an average return of 27.87% per rating and an 85% success rate.

Final Thoughts

Summing up, Alphabet’s Q3 results showed outstanding numbers across the board. All core segments, including Google Search, YouTube, and, most notably, Google Cloud, posted excellent top and bottom-line gains. For this reason, I believe that Alphabet’s shares are undervalued at their current levels. With double-digit revenue and earnings growth set to be sustained next year, as well as in the years to follow, Alphabet stock is still trading at a discount, even after its recent post-earnings gains. Therefore, I will remain invested in Alphabet, now my second-largest personal holding.