{kind=link}

Two weeks ago, the tech industry was abuzz with the news of Alphabet, Google’s parent, trying to acquire cloud security startup Wiz for around $23 billion. It was to be Alphabet’s largest acquisition ever, 85% more than the amount it paid for Motorola Mobility in 2011, and four times more than it paid for Mandiant, another cybersecurity firm. For Wiz, the price was almost twice its most-recent valuation. However, Wiz turned down the offer, and the deal collapsed. The drama highlighted not only the strategic interests of Google, but also some of the big issues facing the tech industry.

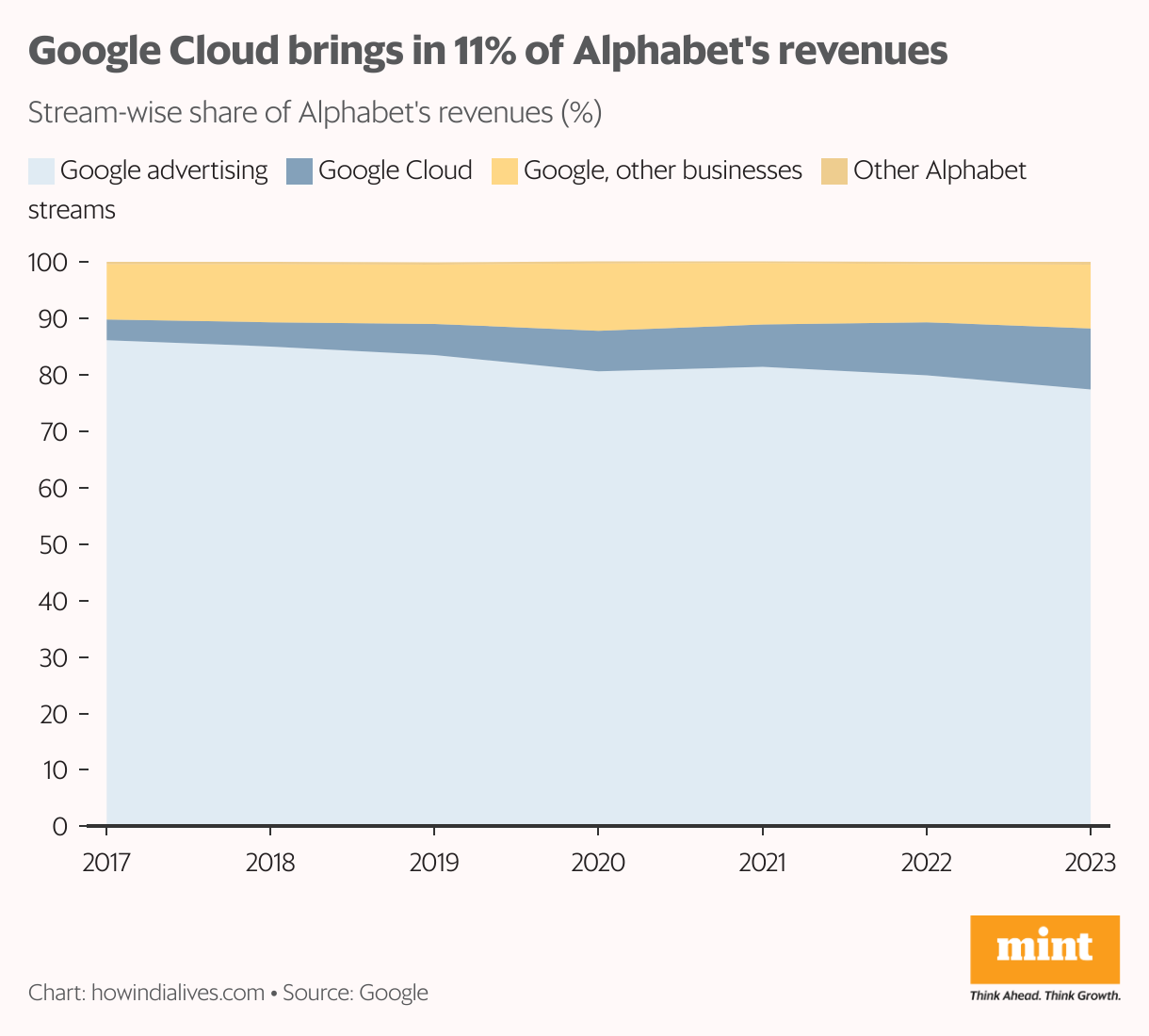

Over the past few years, Google, which gets most of its revenues from advertising, has been trying to strengthen its other revenue streams. As a result, the share of its cloud business in its total revenues increased from 3.7% in 2017 to 10.8% in 2023. It’s one of the top three players in the cloud market. But with a 11% share, it trails Amazon, whose AWS has a 31% share and Microsoft, whose Azure has 25%, according to Synergy Research Group.

Acquiring Wiz would have helped Google in two ways. It would have given it an additional revenue stream. Wiz, which is only four years old, reported an annual revenue of $350 million in 2023. It would have also helped Google in the cloud infrastructure business, as customers increasingly prefer dealing with fewer vendors. According to Capgemini, three out of four organisations were already pursuing vendor consolidation in 2022. The trend is only expected to strengthen.

Monopoly woes

While vendor consolidation has been pushing IT companies to acquire startups that offer complementary products, a counter-push has been coming from governments through their anti-competition agencies. When the early news about Google’s intention to buy Wiz came out, there were questions about it getting the deal approved by regulators. Google is already facing two anti-trust trials: one accusing it of illegally monopolising the advertising technology market and another of monopolising the search engine market.

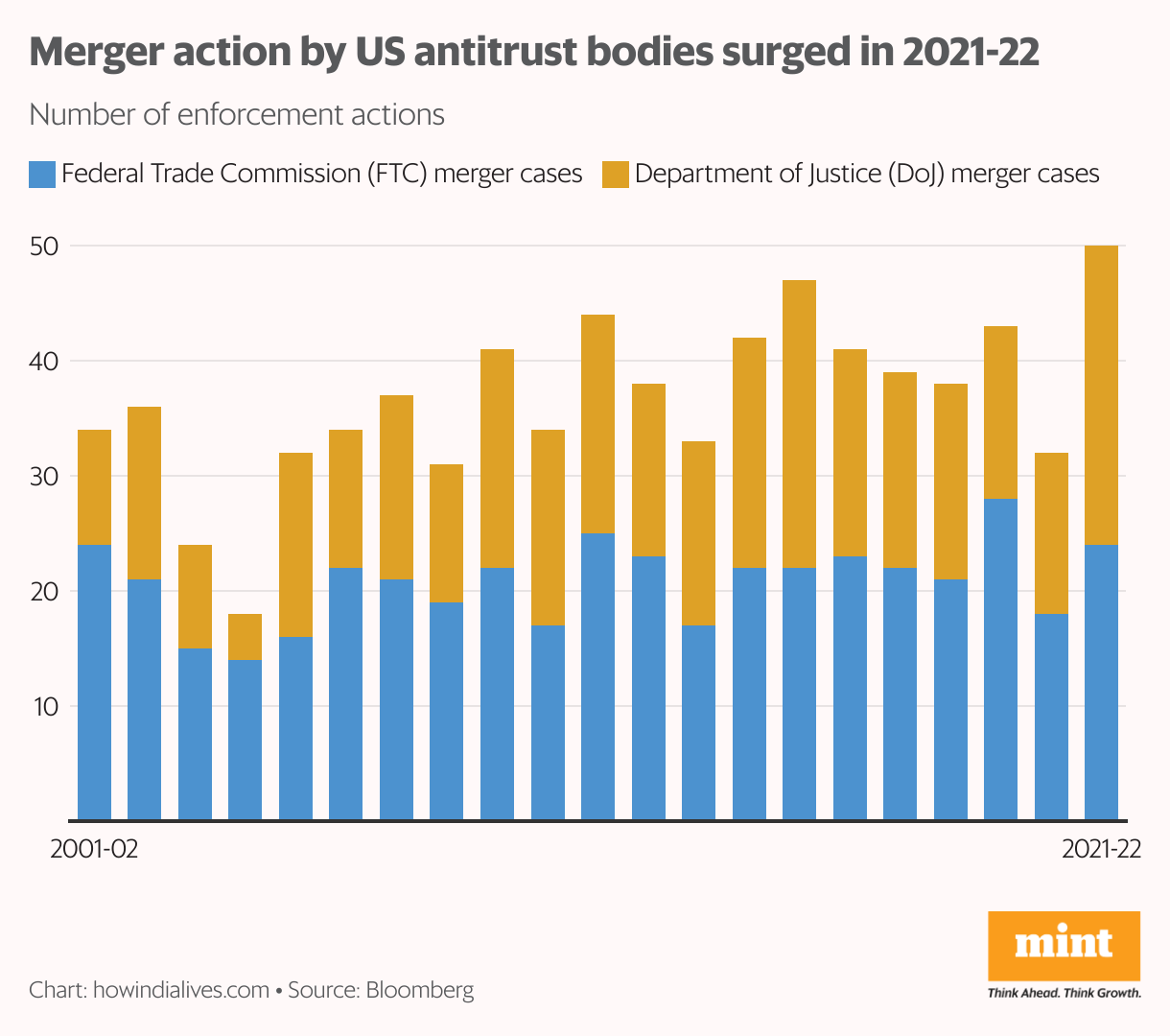

There has been a pushback against mergers too. Last December, Bloomberg reported that merger enforcement activity in the US was the highest in 2021-22 (for which the latest data was available) since pre-merger antitrust reviews started in 1976, with 24 cases filed by the Federal Trade Commission and 26 by the Department of Justice. While companies have won many of these cases, notably Microsoft’s acquisition of Activision Blizzard, anti-trust questions loom large in M&A deals.

Exit options

One reason the startup ecosystem was watching the Alphabet-Wiz deal with interest was the potential fillip it could provide to M&A deals. According to a June report by consulting firm PwC, the number of M&A deals fell by 25% in the first half of 2024, compared to the year-ago period, a downward trend that began in 2022. “The daunting combination of high interest rates, current valuations and political uncertainty has been a showstopper for many deals,” it said.

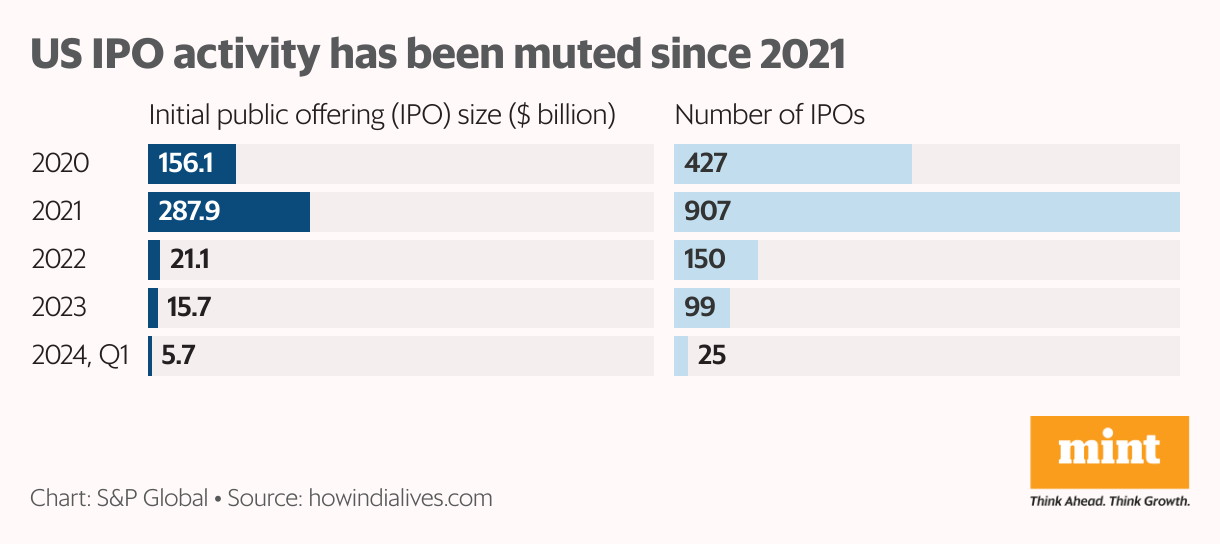

After turning down Alphabet’s offer, Wiz CEO Assaf Rappaport said in a memo to the company staff that it would pursue an IPO. IPOs, another key exit option for investors, have also been down in the past few quarters, both in the US and globally. According to S&P Global, US companies launched 25 IPOs in the first quarter of 2024, up from 23 during the same period in 2023 but far lower compared to 357 in Q1 2021. The IPO market has been slow since 2021.

Cloud opportunity

Wiz’s confidence, despite the muted IPO market, comes from the health of the segment it operates in—cloud security. In just over two years of its founding, it hit an annual recurring revenue of $100 million, and counts 25% of Fortune 100 companies among its clients, a reason why Alphabet was willing to pay a huge premium over its previous valuation. Wiz can now anchor that to command a better price.

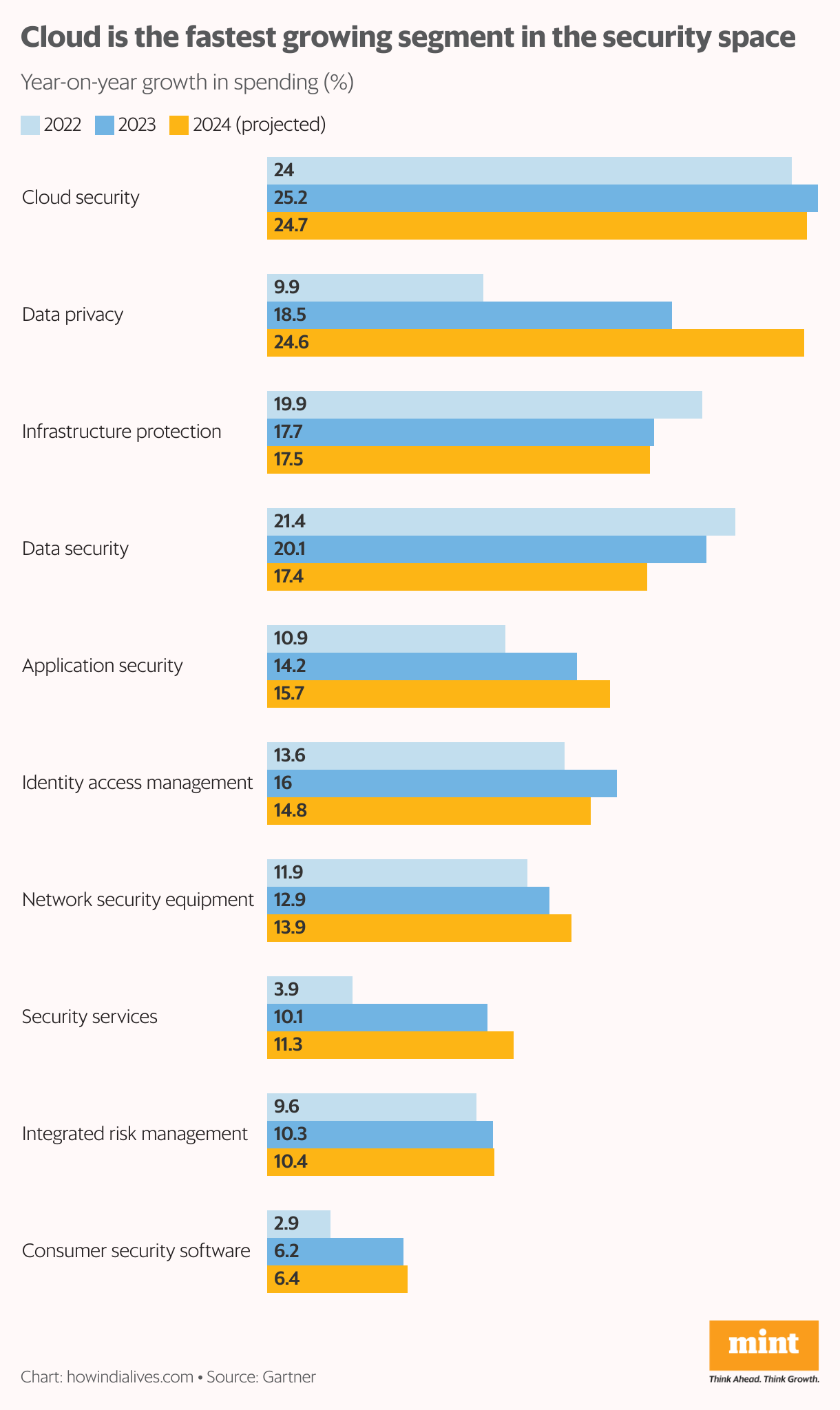

It’s supported by demand for cloud security. According to Gartner, cloud security spending has been outpacing other security products and services in 2022 and 2023, and is expected to do so again in 2024. That, in turn, is driven by the growing cloud adoption. By 2028, cloud computing will shift from being a technology disruptor to becoming a necessary component to maintain business competitiveness, Gartner said last year. Simultaneously, cybersecurity risks are growing. The collapse of the deal is a sign of the potential of the cloud security market.

www.howindialives.com is a database and search engine for public data.

Also read: Cybersecurity: Microsoft’s Azure woes and Google’s acquisition moves